Is it time to think beyond sales?

As a real estate agent, have you ever though about what your exit strategy would look like? When you’re too old, or too tired, or just lose the passion for the sale, what’s next? Do you somehow sell your book of business, move into a related or even unrelated field, or just retire? But is there something more to this? Most of the successful agents we know eventually come to the realization that they want more than a good career… they want to build wealth, serious wealth. Fortunately for them, there is no better way than building wealth through real estate.

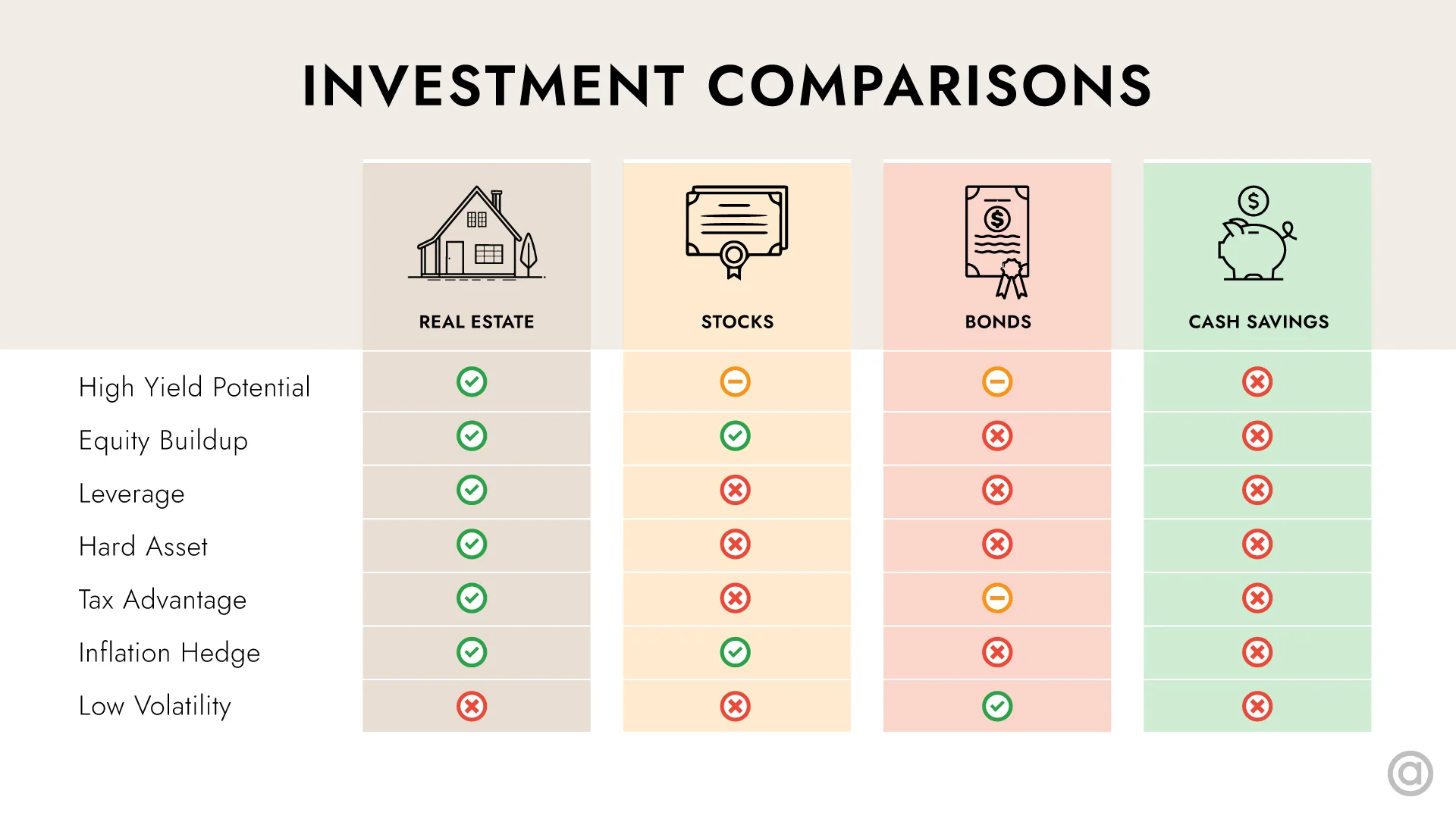

When most people think of building wealth, their minds typically go to four major places – real estate, stocks, bonds, and cash savings. Savvy entrepreneurs understand that there’s a fifth wheel – building or owning businesses, but that’s a conversation for another day. Illustrated below, we’re focusing in and comparing different investment options. It’s easy to see that real estate holds a distinct advantage here, and that’s why we’re focusing in for the purposes of today’s blog post.

Cash is NOT king

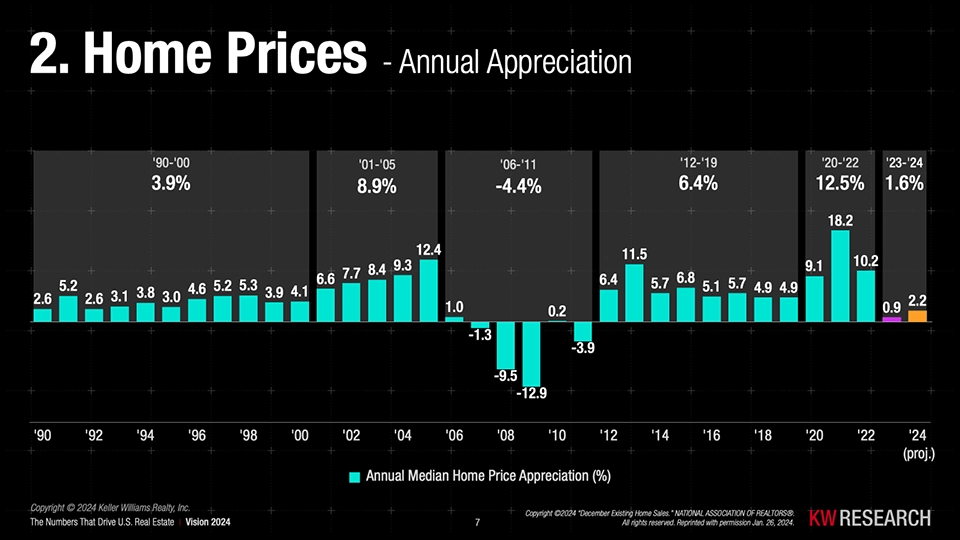

But first, I want to touch briefly on why Robert Kiyosaki, among others, continually repeat that you can’t save your way to wealth. The primary reason is inflation, which I’m sure we’ve all been hearing a lot about lately. As prices rise, the real value of money declines which means that the same amount of cash will buy fewer goods and services in the future. This diminishes the actual worth of savings, causing savers to lose financial ground even if their nominal account balance remains the same or grows slightly.

So when you ‘save’ that $100,000 in a typical savings account, feeling safe and comfortable with the 2% interest that it’s earning, it’s actually misleading. That’s because inflation, currently at 3.4%, is outpacing the rate that your money is earning. That 2% rate the bank is paying you is indeed earning you $2,000 for the year. However with inflation at 3.4%, the $102,000 in your account will now only buy you as much as $98,532 did last year. For savings accounts to be even decent investment vehicles, they would need to be high yield savings accounts that greatly outpace the rate of inflation.

That brings us back to real estate

As a full time real estate agent, investing in real estate should come natural to you. Buying and selling real estate day in and day out should offer you all the encouragement you need to see the endless possibilities that investment in this class offers. Plus, you have a distinct advantage, two really, that makes real estate investment a natural fit:

First – you have front line access to home sellers that want or need to sell their homes. Wouldn’t it an incredible benefit to your clients to say, “We can sell your home one of two ways – we can put it on the market, with all that entails, and let the market determine how much your home is worth. Or… I can give you an as-is offer, and you can avoid the makeready, the photos, the showings, the open houses, and all the headaches that those can bring?”

Second – you have access to the MLS. You have access to research tools like Remine, IgniteRE, and NATSuite. You have access to every CAD database in the state. And all of these tools allow you to taylor your searches ad-nauseam, and directly market to homeowners in ways that the general public can’t, or can’t afford to.

Seven reasons you should invest now

So what makes real estate the greatest path to building your personal wealth? Well that’s easy – because there are seven ways owners can build wealth through the accumulation of real estate assets: Leverage, Cash Flow, Appreciation, Depreciation, Loan Paydown, Forced Equity, and Inflation. We’ll touch on each of these below.

Leverage

Real estate stands along as one of the easiest assets to leverage. With interest rates still hovering in the 6% range, even with 20% down, a 30-year mortgage offers very favorable terms for long and short term rental properties. And by utilizing the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) effectively, you can purchase a property, improve its value, then refinance it to recover all (or even more) of your invested capital. Even if you don’t get back 100%, you can still achieve a fantastic 50-90% return on investment while building equity in the property.

Leverage is a powerful tool in real estate ownership that often gets overlooked. Where else can you borrow from a bank, repay the loan with rental income, and pocket the profit? The key to safe leverage is positive cash flow. Make sure your property generates more income than it costs to own, and leverage itself becomes less risky. Over-leveraging happens when you borrow so much that you lose money every month.

Cash Flow

Cash flow refers to the money you have left over from the rent you have collected after all expenses have been paid on a rental property. Most properties have expenses like a mortgage, property taxes, insurance, maintenance, and property management fees. When your property earns more in rent each month than is paid out in expenses, it has positive cash flow. Likewise, if your property’s expenses are greater than the rent it earns, its cash flow is negative.

Investors that buy property solely betting on price appreciation have a singular exit strategy, to sell at a later date. But that also means they have only one pathway to success – to hope and pray that the property continues to appreciate. Any deviation from this plan almost certainly guarantees that the investor loses money, and in situations where the real estate market takes a dive, these so called investors lost a lot more. Losing money, and in many cases, ultimately lost the property.

Wise investors don’t bet on appreciation. They buy properties based on a fundamental understanding that a property must generate more income than it costs to own. Most investors that I know set a bar for how much cash flow a property must produce, and walk away from properties that can’t reach that metric. This allows them the breathing room to remain largely unconcerned about market fluctuations. If home values dip, they’re safe. And any gains simply give them more options.

Appreciation

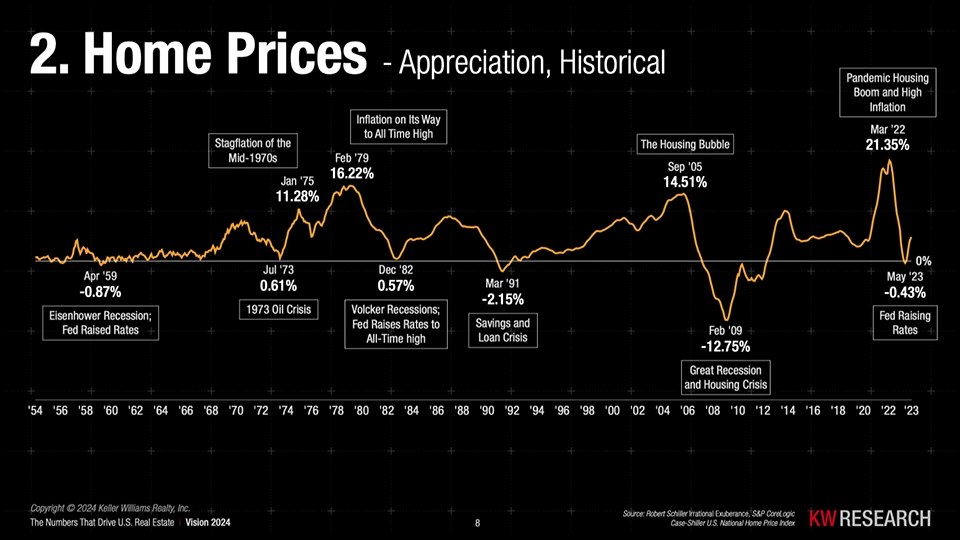

Now, given all of that, appreciation – the rise of home values over time – is how the large majority of wealth is built in real estate. Cash flow pays for the property as well as a modest monthly income, but appreciation is where the large windfalls come from. While home values fluctuate

That said, appreciation, or the rising of home prices over time, is how the majority of wealth is built in real estate. This is the “home run” you hear of when people make a large windfall of money. While prices fluctuate, over the long run real estate values have always gone up, always, and there is no reason to think that is going to change.

Appreciation alone is a big draw for investors over time, but the real home run comes from combining appreciation with leverage. Take for example an investor, who buys a home for $250,000 and it appreciates to $275,000. That equates to a 10% return – not bad, right? But what if that investor used the bank’s money? At 20% down, the investor has only tied up $50,000 of their own money. Now, with the same appreciation, they’ve actually earned a 50% return. That’s life changing.

Depreciation

How can both appreciation AND depreciation be a benefit of investing in real estate? We get asked that question a lot. It’s misleading because term depreciation, in the real estate investment world, does not refer to the value of real estate dropping. It’s actually part of the tax code that gives you the ability to write off part of the value of the property itself each year. The benefit comes in the form of a significantly reduced tax burden on the money you do make.

Depreciation on a rental property allows real estate investors to deduct the property’s cost over its useful life, which the IRS defines as 27.5 years for residential rental properties. This deduction helps to reduce the investor’s taxable income each year. So if we take the hypothetical property that we described above – one purchased for $250,000 – we’d divide the purchase price by 27.5 and get $9,091. This is the amount that we could then write off against the cash flow earned on this property this year. Often times, the write-off is greater than the sum total of the cash flow earned and the investor avoids taxes completely.

As always, consult your CPA for more information, but the takeaway here is that the government takes into consideration that real property degrades over time, and gives you the opportunity to claim write-offs for that wear and tear. This benefit does NOT apply however to your primary residence. Tax on rental properties is sheltered because it’s considered business income against which you can claim write-offs. No such benefits exists for your personal home.

Loan Pay Down

When investors take on mortgages to buy real estate, those loans are usually paid back with the rental income that the property produces. And that’s what makes investment properties so attractive: you earn a monthly cash stipend, appreciation builds automatically, and in the meantime your tenants are paying down your mortgage.

Initially, most of your mortgage payment goes toward the interest rather than the principal. However, as you hold the property longer, increasing amounts start applying to the principal, boosting your equity. Over time, equity builds even faster because you’re paying down the loan while the property’s value appreciates. And that’s over and above the monthly cash flow that the investor is taking from each monthly rent payment.

Forced Equity

Forced equity is a powerful benefit for real estate investors, representing the value added to a property through strategic improvements and renovations. Unlike market-driven appreciation, which depends on external factors such as market trends and economic conditions, forced equity is within the investor’s control. By making targeted upgrades—such as modernizing kitchens and bathrooms, enhancing curb appeal, or adding amenities—investors can significantly increase the property’s value. These improvements not only make the property more attractive to potential buyers or renters but also justify higher rent prices and resale values, thereby boosting the property’s equity.

Additionally, forced equity can enhance an investor’s ability to leverage properties for further investment opportunities. As the value of the property increases due to these improvements, investors can refinance the property at a higher valuation, accessing additional funds that can be used to purchase more properties or invest in other ventures. This process accelerates the growth of an investor’s portfolio and increases their overall return on investment. By actively creating equity rather than waiting for the market to appreciate, investors can achieve faster and more predictable financial growth.

Inflation

Imagine for a moment that you buy a house for the express purpose of renting it out. Over time, most things get more expensive, like groceries and gas (that’s inflation). But with long term, fixed rate mortgages, your mortgage payment usually stays the same. Now, because rents usually escalate over time, and because mortgage payments typically don’t, you as the investor are able to pocket more cash flow. What’s more, the value of the house itself tends to go up with inflation. So, even though inflation can make things seem more expensive, the savvy real estate investor can make it work in their favor.

Back to being a Realtor

Keller Williams is WELL known for being, by far, the best training company in the industry. And Keller Williams understands that our agents should not only by building incredible businesses worth owning, but always building legacies worth leaving. So our training programs don’t only focus on building successful businesses. We’ve built an entire ecosystem around helping our agents to build long term wealth.

So spend your time building your real estate business. But reserve a little time for growing your profit share downline. Then save some time to learn how, and more importantly, actively pursue real estate investments to build for your future. So when you’re ready to walk away from selling real estate, you won’t have to worry about your exit strategy.